Affording style

A confessional on how I spend my money

Overview

I’m writing this as a chapter in the exploration of my finances, which has continued to be an area of growth in my life. It’s vulnerable! Incredibly so, sometimes. But I also believe that airing out some of our financial bullshit and successes is healthy. As a person with entrenched shame around the subject, this feels like freedom.

So, today I will unpack an area that I’m currently wrestling with: how to afford building a wardrobe that feels “me,” while also being mindful of my long-term financial goals.

My budget

Since I am currently rebuilding my wardrobe, I set aside $500/mo for clothing. This might feel like a lot to some people and not much to others. But let me walk you through how I got here.

Rebuilding my wardrobe is important to me. It’s tied to one of my main personal goals for this year: finding my own stylistic voice while maintaining a high level of comfort. Because this is a big goal for me, I am willing to invest my time and money in it.

By the same hand, I also have some lingering credit card debt that I need to pay off (my other main goal for 2024!). Somehow, the debt keeps sitting there over the years, ebbing and flowing, but never completely disappearing. My goal is to pay this debt off slowly and steadily. Here, the goal is also $500/mo.

To make this work, I need to know where my money goes. I use the web app, You Need a Budget (YNAB), to track all my costs. I haven’t always been this organized, but in order to feel like I’m approaching this credit card debt payoff and this wardrobe update sustainably, it was really important for me to know just how much money is going where. I’ll give you a little peek under the hood for last month. This was more or less a typical month for me, barring a $700 emergency vet bill, which I left off of this breakdown.

Approximate budget in January 2024:

Mortgage and utilities: $2,400

Car payment and insurance: $440

Cellphone and internet: $250

Food (groceries, eating out, bars, etc): $1,100

Body (toiletries, prescriptions, clothing, gym membership, etc): $1,000

Mind (therapy, entertainment, media, art supplies, etc): $1,100

Giving back (recurring/one-off donations, gifts for others): $400

Miscellaneous costs (gas, flights, household needs, etc): $1,000

Credit card payments: $500

Looking at this list in its totality, I can even now identify areas that I would like to cut back. I wish I could get the “Mind” category shaved down a bit, but in full transparency therapy runs me $860/month and at this point in my life, that’s a non-negotiable expense for me. Having the right therapist makes all the difference. However, I can see how I might pull a few hundred out of “Food” and “Body” (how is skincare so expensive?) to put toward the cc payments. It’s a game of balances.

I can see how the most “responsible” thing to do would be to stop all my frivolous little purchases of kombuchas and old sterling rings from the $25 tray at the antique shop and beeswax taper candles and put that money towards my credit card payment. Perhaps I will make some of those cuts!

Another “responsible” thing to do would be to take the $500 for my wardrobe and put that towards the credit card. But I’m not going to. I have to pick and choose my battles. And I know from experience that cutting out too many of my frivolous purchases makes me bitchy and depressed and ultimately more likely to blow money on a big impulse purchase as a treat for surviving my “ascetic lifestyle” for three weeks.

I admit that I want to feel like I’m getting some material benefits out of working this intense job that pays me more money. It’s a capitalist world and I’m living in it, baby.

How I spend my wardrobe budget

For starters, I have an assumption that I spend more on clothing than many of my friends (this is a spot where some of the shame of feeling “gluttonous” peeks out). I often try to convince myself that I want an expensive garment because it’s made of sustainable materials and it’s high quality and it will last longer. I know how green-washed fashion is, though. And I know that even if a garment has a cool designer’s label on it, it does not automatically mean that the garment’s materials or construction are of higher quality.

Sometimes I want a garment because it’s sustainably made; often I want the garment because it looks cool or fulfills some niche corner of my identity expression. I think that’s ok. I’m no purist and I aim to avoid any approach that appears dogmatic.

To build up my wardrobe, I first had to identify what was missing. Perhaps I’ll get into this aspect another time, but so many have written about it that I doubt I have anything interesting to add to the discourse. Check out Subrina Heyink here on Substack or Nic Seligman on instagram or “The Creative Pragmatist” by Amy Smilovic (founder of Tibi) if you’re curious about how to evaluate your wardrobe needs.

After I identified what I needed, I started to compile a list of links to items that would help me fill some of my wardrobe gaps. This quickly developed into a spreadsheet where I track the clothes I want, why I want them, how badly I want them, and whether or not I’ve made a purchase. The spreadsheet helps me get a long-term view of my goals and desires; this very much helps me plan. It also helps me feel confident and excited about the purchases I make.

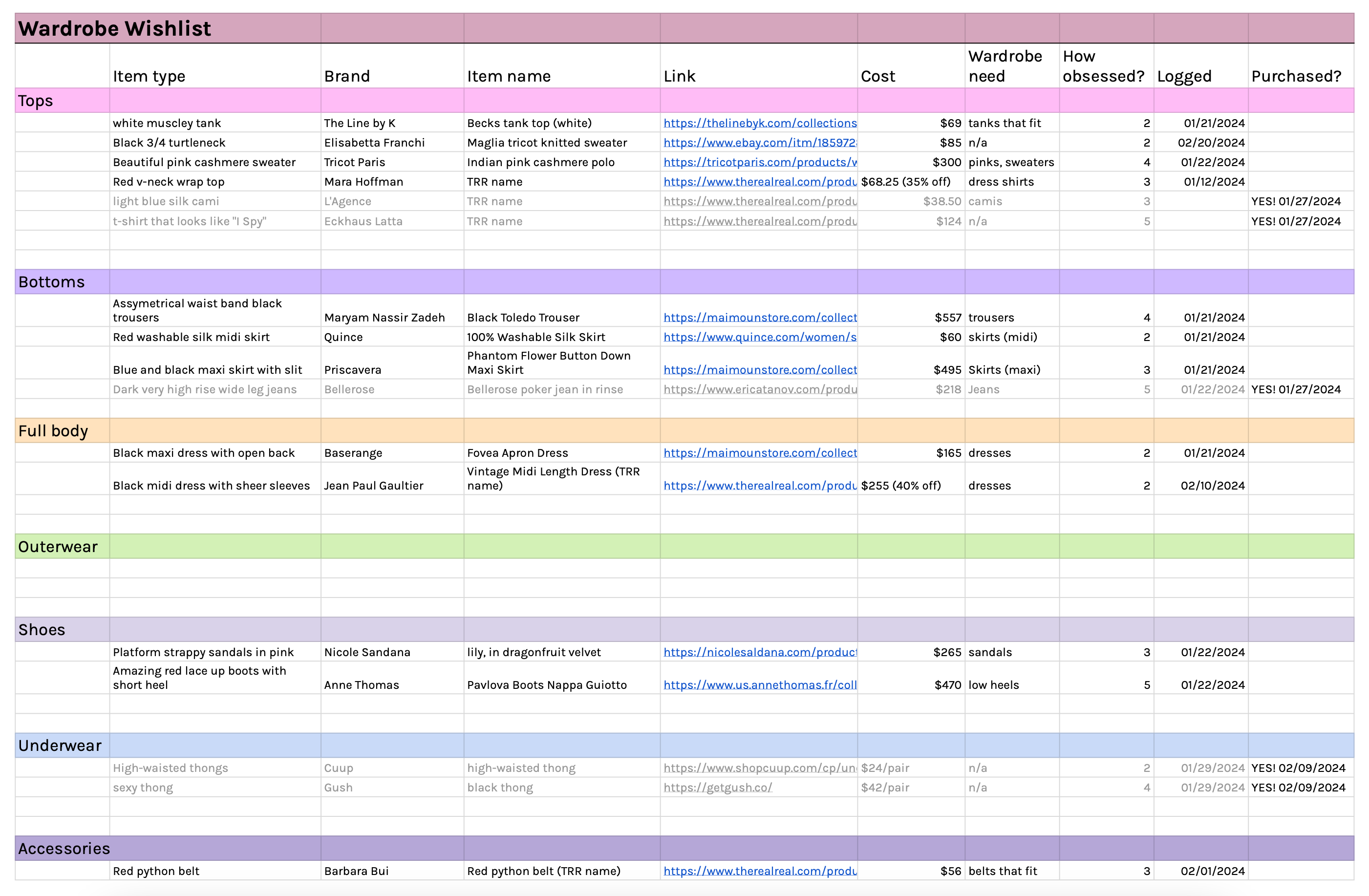

Here’s a screenshot of my current spreadsheet:

If the image is hard to read on your device, here are the criteria I list out for each desired item on the spreadsheet:

Description of item

Brand

Item name, if applicable

Hyperlink to item

Price

Wardrobe need this item fulfills

Level of excitement (1–5)

Date of initial entry

Date of purchase, if applicable

If an item is more than my budget for an entire month, I ask myself if I really need it. And if I really do think I’ve gotta have it, I plan accordingly. Anything spent above the month’s budget comes out of the next. YNAB makes that easy to track, otherwise I think I’d “forget” to carry over any extra costs to next month’s budget.

I should also mention that I do the vast majority of my shopping online. I live quite far away from any cool shopping districts and I kinda like it that way. I’m far less likely to make an impulse purchase online than I am in person. On the flip side, I’m far more likely to buy something that doesn’t fit right online than I am in person. Online shopping is a gamble I’m willing to take if I can find something at the right price point or there’s a decent return policy. I can imagine that this spreadsheet method would probably fall apart if I was more of an in-person shopper.

Here’s what budgeting looks like in practice.

With my $500 budget for February, I bought:

8 pairs of Cuup underwear for $130 with shipping. This is my go-to for underwear. However, Cuup must have been recently acquired by a fashion conglomerate and the new website experience is real shit. On the good side, I did get each pair of underwear for $11/piece when the regular price is $24/piece. Thus why I bought so many. My dog destroys a pair of underwear every other week or so, making this a purchase of necessity for me.

1 pair of Gush underwear for $50 with shipping. Sexy splurge!

1970s Taxco sterling silver belt for $300. I’d been looking for something of this style after noticing that I only have incredibly gaudy looking belts that I can wear with dresses, etc. I found this belt at the antique shop and impulse purchased it, as I hinted I’m wont to do. It was more than I would have expected myself to spend on a belt, but I have a real soft spot for cool, functional antiques. It immediately broke while I was still in the store (lol), so the clerk gave me $30 back, which was the exact amount it cost to have it fixed a few days later. Worked out fine and I love it!

What I didn’t buy because I spent my money on the belt: a cool Andersson Bell top listed on Depop that the seller has offered me a discount on several times. It has since sold. Having a clear sense of my budget makes it easier to say no to these spur of the moment offers, especially when the money is already spent for the month.

I hope this was interesting, if not helpful! The taboo nature of talking about money has been a major topic for me over the past year. There can be a lot of shame around how we choose to spend our money, especially when it comes to non-essential costs. We experience shame if we have financial privilege and we experience shame if we do not. We compare ourselves. I imagine no one is spared from some amount of money shame. May we all find more grounding and peacefulness in this part of our lives.

Thanks for coming on the journey with me! <3

With love always,

Kara

P.S. My therapist has been a real help as I try to better understand my emotional relationship with money. She had me take this quiz through financial therapist, Lindsay Bryan-Podvin’s website, Mind Money Balance, to identify my “money archetype” and it was quite enlightening. More on this another time!

Loved this!!!

This is so cool and refreshing Kara! Thanks for being so transparent! I love the idea of a spreadsheet to track gaps in your wardrobe and your ideas for filling them. I would love to hear and see more about your style (clothing, home decor, etc.)!!